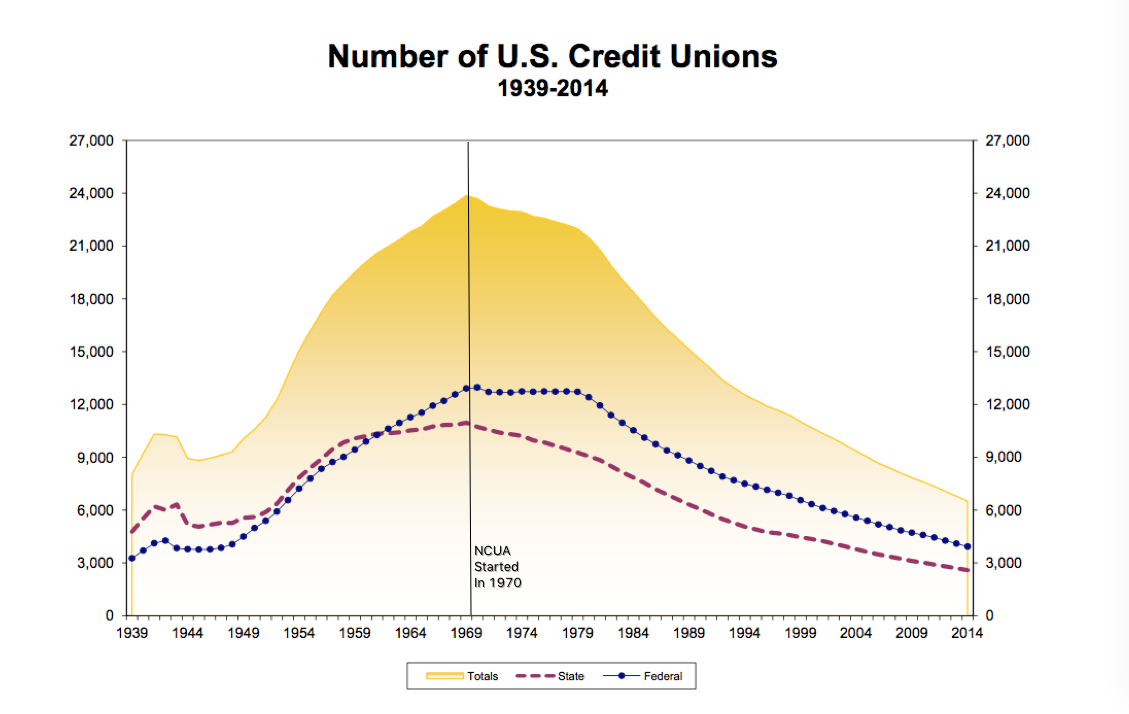

In order to have a growing and sustainable cooperative business ecology you need at least two things: first, you need a continuous stream of newly founded worker-owned firms entering the ecology, either through conversions or as startups; and second, you need a growing cooperatively-owned financial sector in the ecology, to help these worker-owned firms manage their capital. The Kibbutz experience in Israel has shown that, given the chance, capitalist banks will use their financial leverage to force cooperative businesses to adopt capitalist structures over time; in other words, for purely ideological reasons, capitalist banks have been shown to use restrictive loan terms to progressively force cooperatives to convert back into capitalist businesses. (Simons and Ingram 1997) Capitalist banks don’t trust cooperatives, they don’t like to work with them, and when they do, they often insist that cooperatives restructure themselves to operate more like capitalist businesses as a precondition for loaning cooperatives money. A healthy cooperative economy requires a financial sector that shares its cooperative structure and philosophy so that worker-owned firms have access to investment capital from banks that understand what cooperatives are about and on terms that fit the worker-owned business model. That’s why it is so discouraging to see that the number of credit unions in the United States continues to drastically decline:

Source: The Credit Union National Association via the Internet Archive Blog.

Source: The Credit Union National Association via the Internet Archive Blog.

This data was compiled by the folks at the Internet Archive. In 2011, one of the founders of the archive, Brewster Kahle, launched a new credit union, the Internet Archive Federal Credit Union, explicitly to offer low-income members affordable financial services. Sadly, after a frustrating five years, Kahle and his partners have recently decided to close the project, and they blame the regulatory body, The National Credit Union Administration, for putting so much needless regulatory bureaucracy in their way that the credit union never managed to get off its feet. By the Archive’s estimates, 200-300 credit unions are forced to close each year in the US and only a tiny handful are allowed to start. Whatever the problem, from the evidence above it is clear that something is very wrong.

Someday, if we ever achieve a sustainable global cooperative economy, much of the change required will be ideological, but much will also be structural. Among the structural changes, it is clear that the laws that govern credit unions need to be re-written, at least in the US and undoubtedly elsewhere, so that they encourage rather than discourage the foundation of cooperative financial institutions. As Kahle points out in his blog post, the technical tools required to start a cooperative bank have never been easier to use. There is really no technical reason that the curve above should be going down. Indeed, by all rights, given internet-based technical advances in providing financial services, it should be going up, and after the catastrophe of the last global recession — caused in large part by the capitalist financial sector — there is even more reason to see that the cooperative financial sector starts growing again.

Kahle, Brewster (2015) “Difficult Times at our Credit Union.” Internet Archive Blogs, blog.archive.org, 24-11-2015.

Popper, Nathaniel (2015) “Dream of New Kind of Credit Union Is Extinguished by Bureaucracy.” New York Times, 24-11-2015.

Simons, Tal and Ingram, Paul (1997) “Organization and Ideology: Kibbutzim and Hired Labor, 1951–1965.” Administrative Science Quarterly 42, 784–813.

Via Boingboing.com.